Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Why Everyone Is Talking About West Orange Right Now: Major Developments Shaping the Community

West Orange has long been one of Essex County’s most desirable places to live, thanks to its beautiful neighborhoods, excellent parks, convenient location, and vibrant community. Now, a wave of exciting new developments is making the township even more attractive for residents, businesses, and homebuyers alike.

From the opening of a brand-new Target to the arrival of Trader Joe’s and continued redevelopment projects throughout town, West Orange is investing in its future—and residents are beginning to see the results.

Here’s a closer look at what’s happening around town.

A New Target Has Transformed West Orange Plaza

One of the biggest recent additions is the new Target at West Orange Plaza. The store has completely transformed the former K-Mart location into a modern shopping destination that serves residents throughout West Orange and neighboring communities.

The addition of Target brings greater convenience for local families while attracting more visitors to the plaza, helping support nearby businesses and restaurants.

But Target is only the beginning.

West Orange Plaza is currently undergoing a broader redevelopment designed to create a more vibrant and pedestrian-friendly shopping experience. Plans include new retail buildings, expanded restaurant options, outdoor gathering spaces, and improved walkability throughout the center.

Several exciting businesses are expected to join the plaza, including:

- Club Pilates

- Quickway Japanese Hibachi

- Namkeen Hot Chicken

- VIO Med Spa

Combined with existing favorites like Whole Foods Market, Chipotle, Jersey Mike’s, and Starbucks, West Orange Plaza is quickly becoming one of Essex County’s premier retail destinations.

Trader Joe’s Is Officially Coming to West Orange

Another exciting announcement is the approval of a new Trader Joe’s location at Mount Pleasant Plaza on Mount Pleasant Avenue.

Trader Joe’s has earned a loyal customer following across the country, and new store openings often generate excitement throughout surrounding communities. Residents frequently travel significant distances to shop at Trader Joe’s, making each location a destination that increases activity for nearby businesses.

For West Orange residents, the new store means another high-quality grocery option alongside Whole Foods, ShopRite, and other local favorites.

Beyond convenience, the addition of Trader Joe’s reflects continued confidence in West Orange as a thriving and growing community.

Essex Green Continues to Evolve

West Orange is also seeing continued investment around Essex Green and other commercial areas.

As businesses renovate, expand, and attract new tenants, these improvements contribute to a stronger local economy and provide residents with more shopping, dining, and entertainment options close to home.

Ongoing redevelopment projects demonstrate a long-term commitment to improving the community while supporting local businesses and enhancing everyday life for residents.

Why These Developments Matter for Homeowners

When people think about buying a home, they’re evaluating much more than the property itself.

Today’s buyers are looking for communities that offer convenience, quality shopping, dining, recreation, and an enjoyable lifestyle.

Access to grocery stores, restaurants, fitness centers, coffee shops, and retail destinations plays an important role in where buyers choose to live.

Continued investment in these amenities helps strengthen West Orange’s appeal, making it an attractive place for families, professionals, and retirees alike.

While no single development guarantees changes in home values, sustained community investment can contribute to a neighborhood’s long-term desirability and support buyer interest over time.

default

A Bright Future for West Orange

Taken together, these projects paint an exciting picture of where West Orange is headed.

The opening of Target, the arrival of Trader Joe’s, continued redevelopment at West Orange Plaza, and ongoing improvements throughout the township all demonstrate a community committed to growth and progress.

Whether you’re a current resident, considering a move, or simply interested in what’s happening locally, there’s never been a more exciting time to watch West Orange evolve.

Thinking About Buying or Selling in West Orange?

Real estate is about more than just homes—it’s about the community, lifestyle, and opportunities that surround them.

If you’re considering buying, selling, or simply want to learn more about the West Orange market, I’d be happy to answer your questions and help you understand what these exciting developments could mean for you.

Contact Lorie-Anne Phillips

Whether you’re searching for your next home or wondering what your current property may be worth, I’m here to help you navigate the West Orange real estate market with confidence.

Could Co-Buying Be the Answer for Some First-Time Buyers?

For a lot of would-be first-time buyers, affordability is the thing that’s standing in the way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying.

The Dream Is Still Alive. The Math Just Isn’t Working for Everyone.

Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation.

The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases, the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981.

But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door.

So, What’s Co-Buying?

Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner.

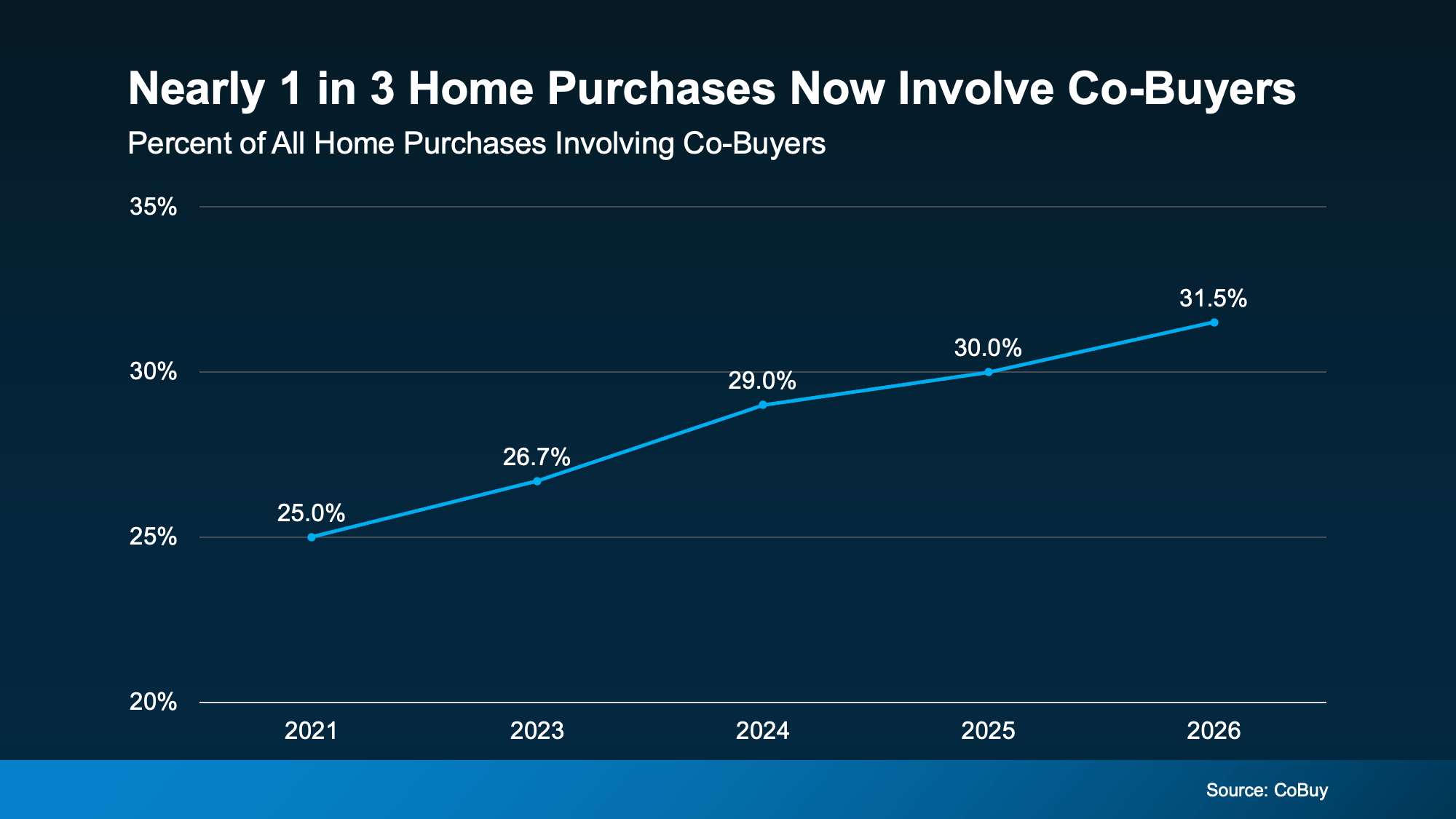

And it’s catching on fast, just look at where things stand today. According to CoBuy.io, 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below):

Why It Works

Why It Works

Why It Works

Why It WorksHere are just a few of the top reasons buyers are going this route, according to NerdWallet:

- Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours.

- More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own.

- Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers.

- Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting. Plus, sharing costs can make repairs or renovations more manageable, too.

Things To Keep in Mind

If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road.

That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment.

Bottom Line

Affordability challenges are real, but they don’t have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots.

If you’re curious whether it could work for your situation, let’s talk. Reach out today and let’s figure out your path to homeownership together.

3 Must-Do’s for First-Time Home Buyers

Buying your first home is exciting, but it can also be a little nerve-wrecking because it’s something you’ve never done before. And trying to think of everything you need to do can feel like a lot. But here’s the key.

You don’t have to figure everything out on your own. And you don’t have to do it all at once. Just tackle it one thing at a time.

Here’s a simple list of 3 main things you should focus on to help you get started.

1. Assemble Your Team: Don’t Do This Alone

Buying a home is a team sport. And having the right professionals by your side can make a world of difference. Here’s who you need to find:

- A local real estate agent is your guide from the first showing to closing day. They’ll make sure you understand all the details along the way, so you feel confident in your decision.

- A trusted lender will walk you through loan options, monthly payments, and what’s realistic for your situation. That information is something you’re going to want early on.

2. Prep Your Finances: Set the Foundation First

This is what determines what you can afford, how competitive you’ll be, and how confident you’ll feel when it’s time to make an offer. Here’s how to get ready:

- Check your credit score. Your credit score impacts the loan options you’ll qualify for and even the mortgage rate you’ll get. Knowing this number early gives you time to work on raising your score, if you want to.

- Save for your down payment and closing costs. Most buyers focus on the down payment, but closing costs matter too. Having savings set aside for both helps you avoid last-minute stress and surprises.

- Look into assistance programs. Many first-time buyers qualify for programs that’ll give their homebuying savings a boost. This can make buying possible sooner than you expect.

- Talk to a lender about mortgage options. Fixed-rate, adjustable-rate, FHA, VA, and conventional loans all work differently. Understanding the options helps you choose what fits your goals best.

- Get pre-approved. A pre-approval tells you what a lender would be willing to give you for your home loan. This’ll help you figure out your price range and set you up to move fast when the right home comes along.

- Figure out your budget. Your mortgage is just one part of homeownership. Budgeting for your utilities, home insurance, and everyday expenses and maintenance will help make sure your payment feels comfortable, not stressful.

3. Gather Your Documents: Save Time (and Stress)

When you’re officially ready to kick off the buying process, lenders are going to need to verify your income, assets, and financial history. Having these documents ready-to-go upfront can speed up the process and reduce back-and-forth. Here’s what Bankrate says you need to prep:

- W-2s and tax documents (past 2 years). These show income stability and help

- Recent pay stubs (generally the past 1–2 months). Pay stubs confirm your current income and employment status.

- Bank statements (past 2–3 months). These show your savings, spending patterns, and where your down payment funds are coming from.

- Investment account statements (past 2-3 months). If you’re using investments as part of your financial picture, lenders may ask for these as well.

- Copy of your driver’s license. This verifies your identity and is required for loan processing.

- Residential history (past 2 years). Lenders use this to confirm stability and background information.

- Statements for any outstanding debts (past 2 months). Student loans, auto loans, and credit cards affect your debt-to-income ratio, so lenders will want to know about them.

- Proof of supplemental income. Bonuses, commissions, side work, or child support may count toward your income if documented properly.

Note: the exact time frames and list of documents may vary lender to lender. This is just a general rule of thumb to help you get the ball rolling.

Bottom Line

Buying your first home doesn’t mean you have to have everything figured out. It just requires a plan.

If you start with your finances, organize your documents, and surround yourself with the right people, you’ll be in great shape when the time comes to make a move.

And if you want more information on anything in this list or just need help getting started, don’t hesitate to reach out.

Should You Wait for Lower Rates?

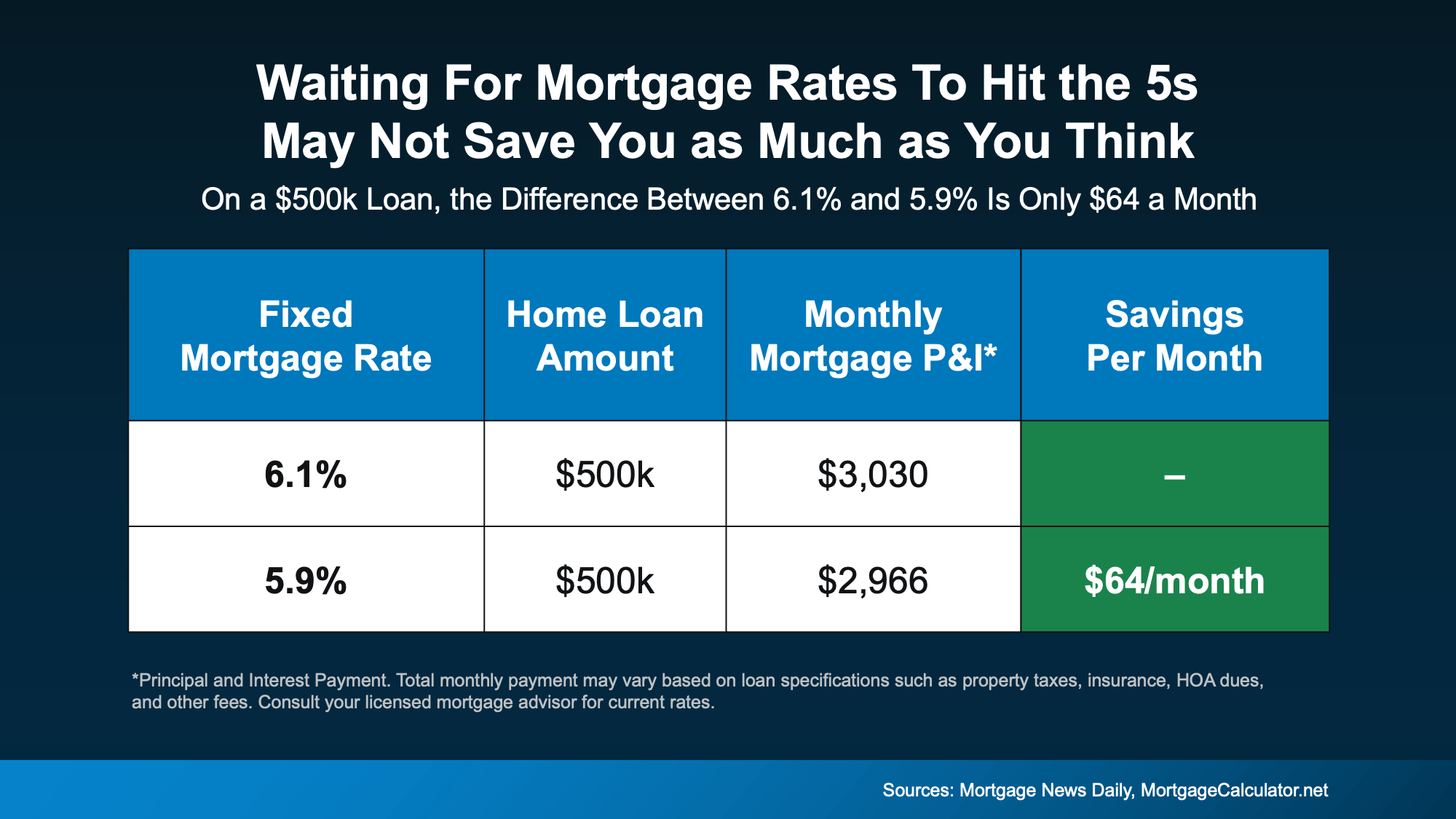

Mortgage rates have already dropped into the upper 5s twice this year. But after just a few days, they ticked back up into the low 6% range. If you saw that and thought, “Great. I missed it,” you’re not the only one.

A lot of buyers are treating the 5s like some kind of magic number. As if moving from 6.1% to 5.99% suddenly changes everything. And from a mindset perspective, it does feel different.

But here’s the part most people don’t actually run the math on.

The Payment Difference Isn’t What You Think

Let’s say you’re looking at a $500,000 home loan. At 6.1%, generally speaking, your principal and interest payment is roughly $3,030 per month. At 5.9%, it’s about $2,966 per month.

That’s a difference of only $64 a month.

Not $300.

Not $500.

Sixty dollars.

Let that sink in for just a moment.

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

Yes, over time that $64 a month can add up. But it’s far from the dramatic swing many buyers imagine when they say they’re “waiting for the 5s.”

The psychological impact of seeing a 5 in front of your rate can feel big. The financial impact? It might be something you don’t even notice when it’s all said and done.

Experts Aren’t Predicting a Big Drop

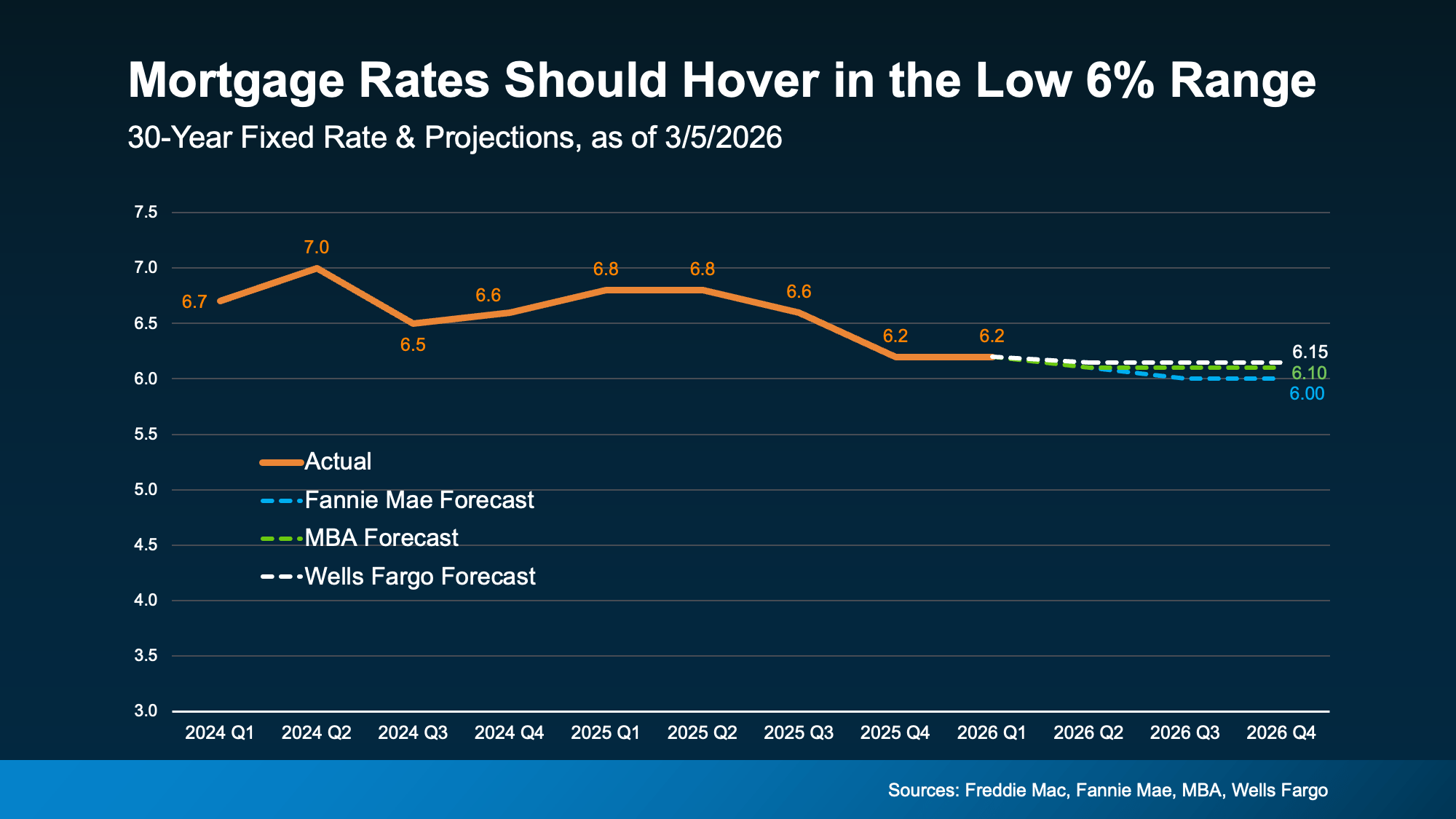

Another important piece to think about: most housing economists aren’t forecasting a long-term return to 5% territory anytime soon.

While rates will move up and down, likely hitting the high 5s here and there, the broader expectation is for mortgage rates to hover in the low 6% range this year, not stay in the 5’s or decline much more.

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

While it certainly could happen, the reality is, waiting for a deep drop may not deliver the payoff you’re hoping for, if you’re holding out

The Bigger Question to Ask

Instead of asking, “Did I miss the 5s?” A better question is: “Does today’s payment work for me?”

If the monthly payment fits comfortably in your budget, and you’ve found a home that meets your needs, the difference between 6.1% and 5.9% likely isn’t the deciding factor. It might be one of them, but it shouldn’t be everything.

And remember, mortgage rates aren’t permanent. If they drop meaningfully later, refinancing is always an option. But you can’t refinance a home you didn’t buy.

Waiting Might Feel Safe, But It Isn’t Always Strategic

It’s natural to want the best possible rate. Everyone does. But sometimes buyers overestimate how much a rate in the high 5s will change things in today’s market.

Don’t miss the fact that rates have already come down. A year ago, they were in the 7s. Now? They’re hovering in the low 6s. And for a lot of people, that percentage point difference that’s already here is the real game changer.

If you paused your plans when rates were higher, now may be the right time to re-run your numbers. Not because rates are “perfect.” But because the monthly payment math might work better than you think, even with rates in the low 6s.

Before assuming you’ve missed your moment, take another look at the numbers.

You may find it never disappeared.

Bottom Line

If you’ve been sitting on the sidelines waiting for that magic number for rates, that strategy may not pay off as much as you’d expect.

Let’s connect so you can double check the math at your price point. You may realize payments are already within your range.

Renting vs. Buying: The Numbers Might Surprise You

Renting can feel like the easier choice right now. There’s no big down payment. No dealing with surprise repairs. And no long-term commitment.

But then your rent goes up again. And again. And suddenly the thing that seemed flexible starts looking… expensive, especially considering you’re not building any equity. And once that happens, it’s easy to feel a little trapped in the cycle.

That’s because there’s so much chatter today about how buying a home isn’t affordable. But the truth is, the math may work out better than you’d expect based on what’s changed recently.

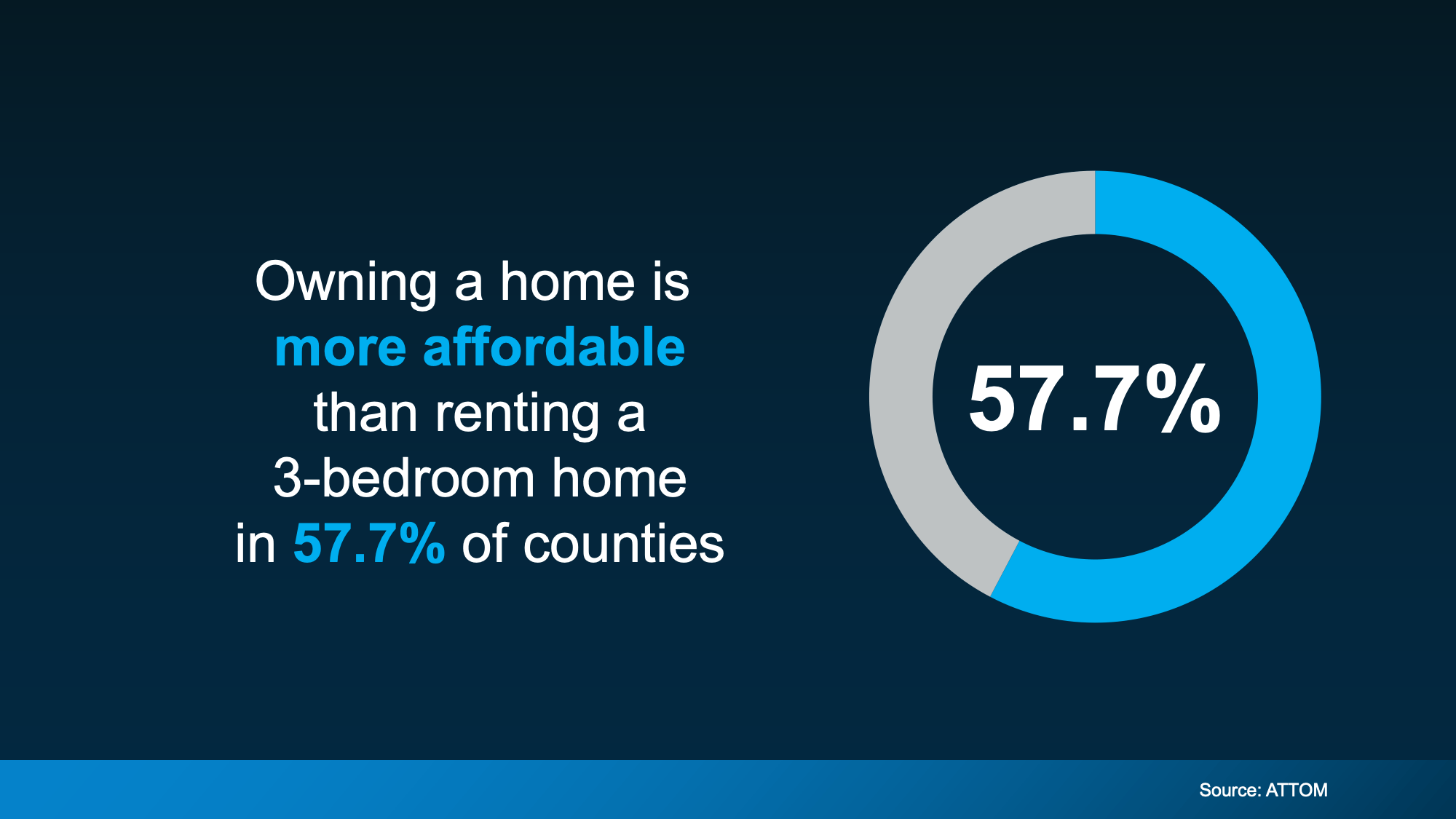

Buying Is More Affordable Than Renting in Many Areas

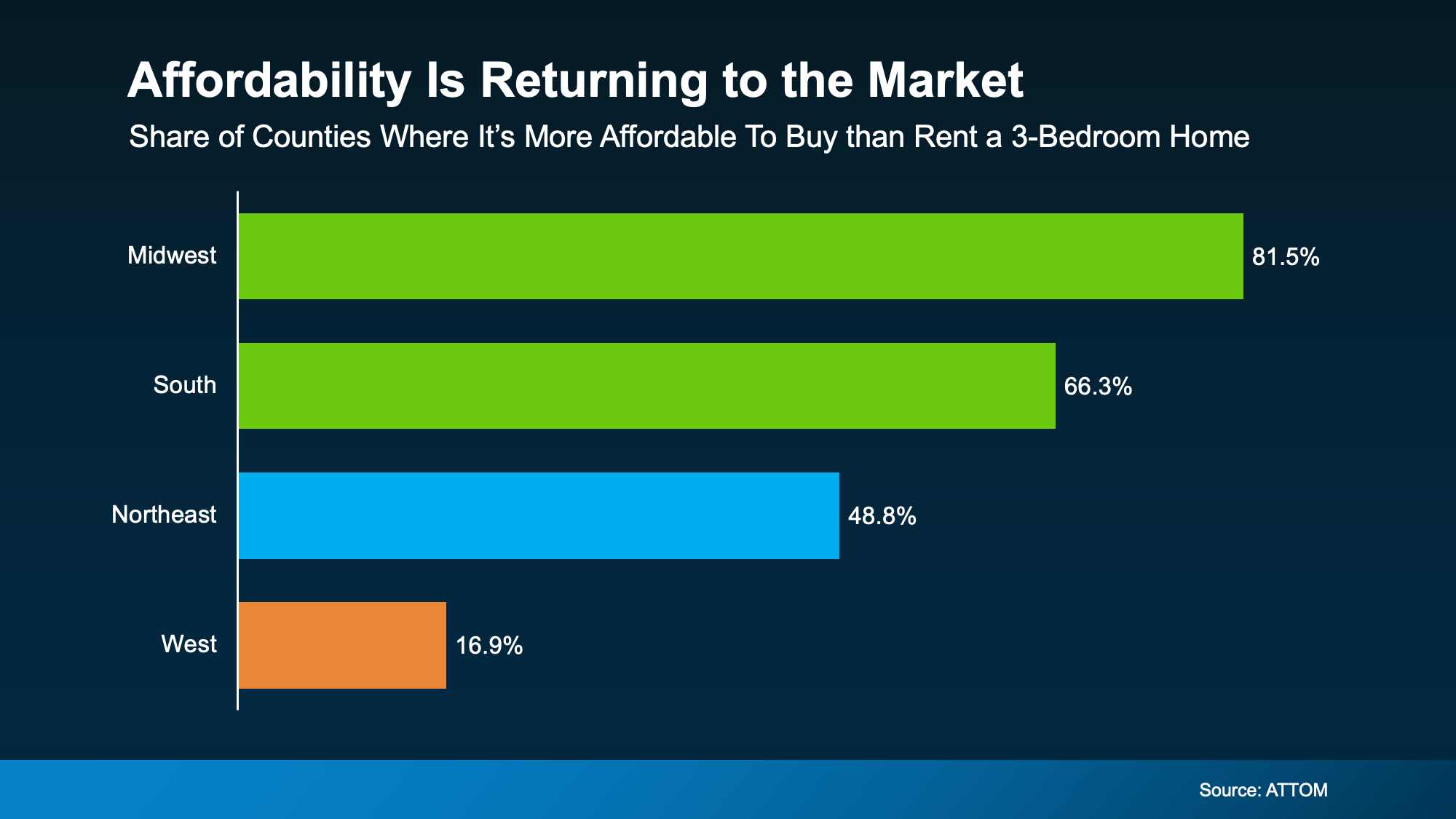

In a lot of places today, owning a home actually costs less each month than renting a 3-bedroom home. And recent data from ATTOM shows that’s true in nearly 58% of counties across the U.S. (see chart below).

And that’s after you factor in things like insurance and typical maintenance costs.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

In other words, even though it may feel like a bit of a shock, the numbers show rent often stretches monthly budgets more than owning does. That’s thanks to slower home price growth, more homes for sale, and monthly mortgage payments starting to ease as rates come down.

Affordability Still Varies by Region

Now, even though nationally the balance has shifted, that doesn’t mean buying is more affordable in every market or for every renter.

While buying is more affordable than renting in nearly 58% of counties nationwide, that share looks different depending on your region (see graph below):

The biggest improvement is happening in the Midwest and South. But if you’re living in the West, things could still feel tight.

The takeaway? How affordable buying is really depends on where you live. And the only way to know how this plays out where you live is to look at the numbers locally.

So, What’s Still Holding Buyers Back?

Maybe you’re nodding along so far but thinking, “Okay, but I still can’t afford the upfront costs.” If that’s your reaction, you’re not the only one.

For many renters, the biggest hurdle isn’t the monthly payment alone. It’s the down payment, too.

But you’re not out of options. Here’s the part most people don’t hear enough about: there are thousands of down payment assistance programs available across the country, and many buyers qualify without realizing it.

And the average benefit? Roughly $18,000.

That kind of support can help cover part of your down payment or closing costs, which means you may not need to save nearly as much as you think to get started.

When you combine that with monthly payments that may work better than expected, especially as rates continue to ease and prices cool, buying may feel far more realistic than it looks at first glance.

Bottom Line

The point isn’t that everyone should rush out and buy a home tomorrow.

It’s that renting isn’t always the more affordable option people assume it is – and buying may be more realistic than it feels once you look at the full picture.

If you’re renting and feeling stuck in the “someday” loop, it might be worth a simple conversation. Just a chance to see what’s possible and whether it makes sense for you.

Move-Up Buyers Are Choosing New Construction

At some point, a house that once felt perfect just… doesn’t anymore.

Maybe you need more space.

Maybe working from home turned your dining room into a permanent office.

Maybe the layout just doesn’t match how you live now.

If your current house is starting to feel like it’s holding you back instead of supporting your life, it’s natural to think about making a move. But that brings up the next big question: once you sell, where do you go?

For a growing number of buyers, the answer is something brand new.

New Construction Is a More Popular Choice Lately

According to the National Association of Realtors (NAR), more people are buying new homes than they have in years. The latest annual data available shows 16% of homes purchased were newly built.

At first glance you may not see why that’s a big deal. But that’s actually the highest share of new home purchases in almost two decades.

Why More Buyers Are Choosing a Brand-New Construction

For many buyers, especially move-up buyers, new construction isn’t just about aesthetics. It’s about lifestyle, convenience, and peace of mind.

1. Everything Is Brand New

You’re not inheriting someone else’s projects. No wondering how old the roof is. No budgeting for a new HVAC right after move-in. No big surprises when the previous owners patch job fails. For move-up buyers who’ve been dumping money into updating their current house, that’s a win.

2. You Can Customize Before Move In

If you choose a home that’s still under construction, you could have the chance to pick the flooring, counters, cabinets, hardware, lighting, and so much more. That level of personalization can be a draw for move-up buyers like you, because it allows you to hand pick the fit and finishes you’ve been wanting for so long.

3. A Home Designed for How People Live Today

Most new construction homes are built to current building standards and buyer preferences, which means you could see built-in smart home features, better energy efficiency (which can lower utility bills), and even more modern floor plans and features. And if your layout just isn’t working for you anymore, you may find exactly what you need now in a new home.

4. Neighborhood Amenities

New developments often include shared community spaces like walking trails, parks, playgrounds, or even pools and gyms. For families and active households, that’s a big bonus to have that just a few steps out of their front door.

5. Builder Incentives

Not to mention, since there are more new homes on the market than the norm, builders are motivated to sell what they have. So, you may find they’re more willing to negotiate than you’d expect on things like price, upgrades, and more.

Bottom Line

If your current house isn’t meeting your needs anymore, don’t assume your only choice is an existing home. New construction is becoming a real contender, especially for move-up buyers who want space, features, and a home that works for how they live now.

Curious whether new construction might be a fit for you? Let’s chat.

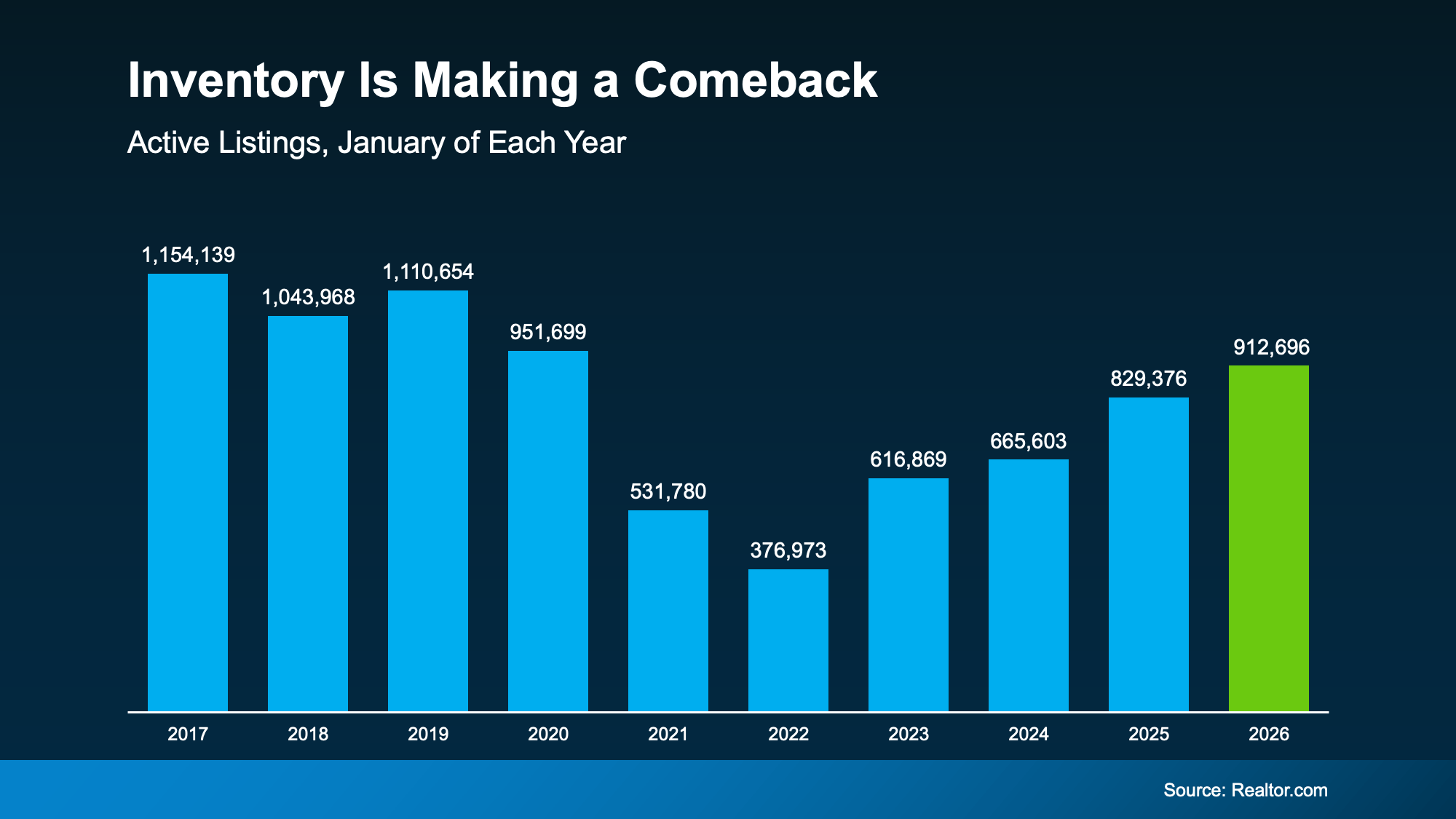

Inventory Is Making a Comeback in 2026

After a long stretch where buyers were competing for too few homes, inventory has made a comeback over the past year. And depending on where you live, that’s opening up your options in a meaningful way.

According to Realtor.com, the number of homes available for sale in January was the highest it’s been since 2020. Here’s why that’s such a big deal. Getting back to pre-pandemic levels signals a slow and steady return to what’s typical:

Now, it’s worth noting, nationally we’re not there yet – and having more inventory improving won’t suddenly “fix” the market. But the growth we’ve seen lately still changes how competitive the market feels.

Now, it’s worth noting, nationally we’re not there yet – and having more inventory improving won’t suddenly “fix” the market. But the growth we’ve seen lately still changes how competitive the market feels.

- When there are more homes for sale, buyers gain time, options, and leverage.

- When there aren’t, the pressure ramps up quickly.

In the years since 2020, there weren’t enough homes for sale, and that made the market feel different. Rushed. Stressful. Intimidating.

But now it’s finally getting better.

A Growing Portion of the Country Is Getting Back to Normal

Depending on where you live, inventory growth is going to vary. Some places are bouncing back faster than others. According to Lance Lambert, Co-Founder of ResiClub, in January 2025, just a little over one year ago, only 41 of the 200 largest metros were back to normal inventory-wise.

But around the end of year, almost half (90) of the largest 200 metro areas were back at or above typical levels. That’s a big improvement in roughly a year. And it’s not done yet.

Inventory Is Expected To Keep Growing

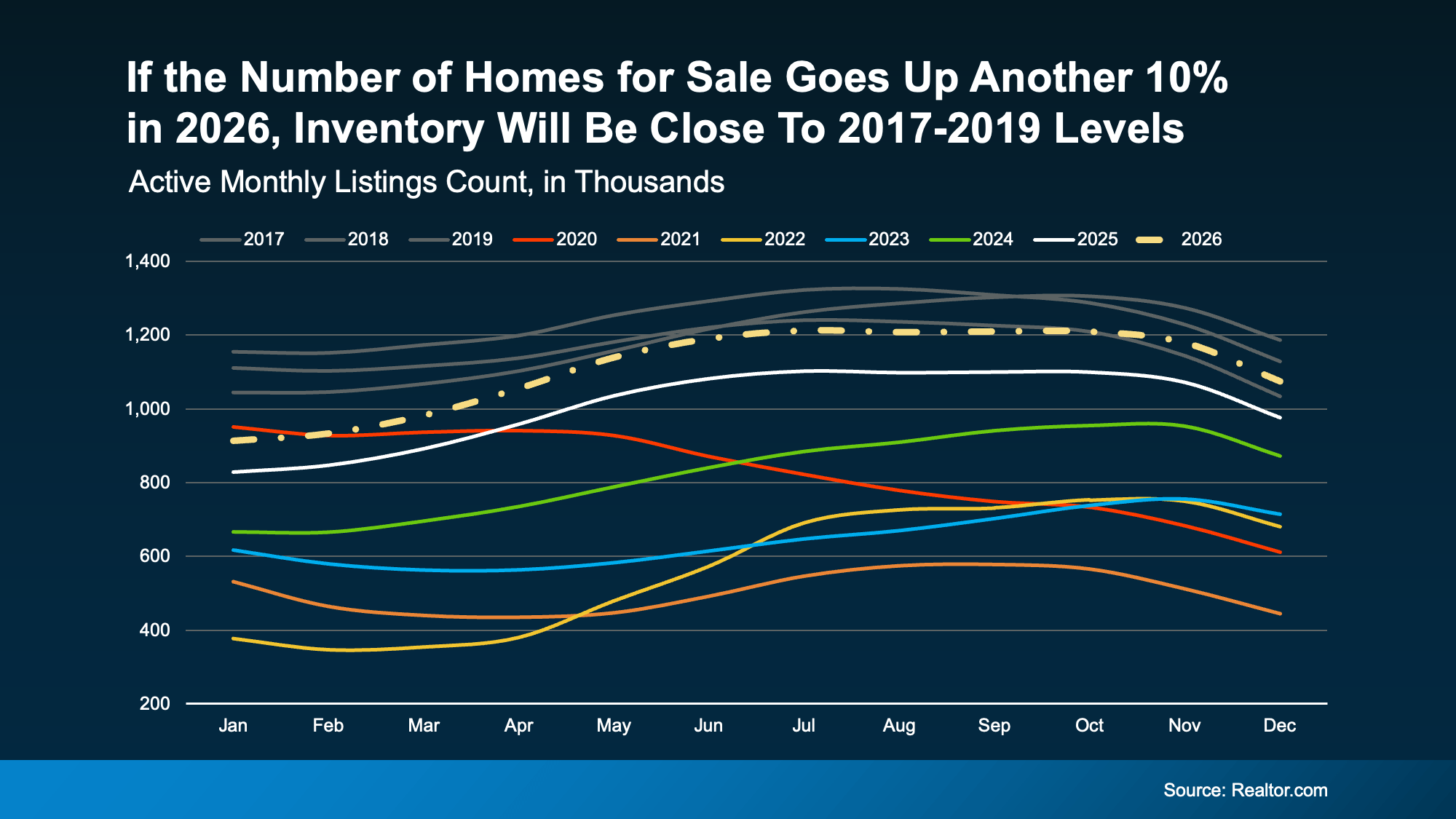

Looking ahead, forecasts suggest the number of homes for sale could rise another 10% this year, which means even more markets should join the list of places where supply has rebounded.

Here’s a graph that shows what an extra 10% would do for the market this year. You can see that projected growth (shown in the dotted line) hits inventory levels seen in 2017-2019 by roughly this fall (the gray lines). That means we may reach normal by end of year, nationally:

And that changes your home search in a good way. As Hannah Jones, Senior Economic Research Analyst at Realtor.com, puts it:

“. . . housing market conditions are gradually rebalancing after several years of extreme seller advantage. Buyers are beginning to see more options and modest negotiating power as inventory improves . . .”

In other words, the market is starting to work with buyers again — not against them.

Bottom Line

Inventory isn’t fully back to normal everywhere. But it’s moving in the right direction. And, in some areas, it’s already there.

If you’ve been waiting for a moment when you have options and a little breathing room, this is the strongest setup buyers have seen in a long time.

If you want to know what’s happening in our local market, let’s talk.

Top 3 Reasons To Buy a Home Before Spring

If you’re planning to buy a home this year, you may be focused on the spring market. And hoping that when spring does hit, you’ll see:

- Mortgage rates drop a little more.

- More homes hit the market.

But here’s what most buyers don’t realize. Buying just a few weeks earlier could mean paying less, dealing with less stress, and feeling less rushed.

Here are three reasons why accelerating your timeline over the next few weeks could actually be a better play.

1. Holding Out for Lower Rates May Not Pay Off

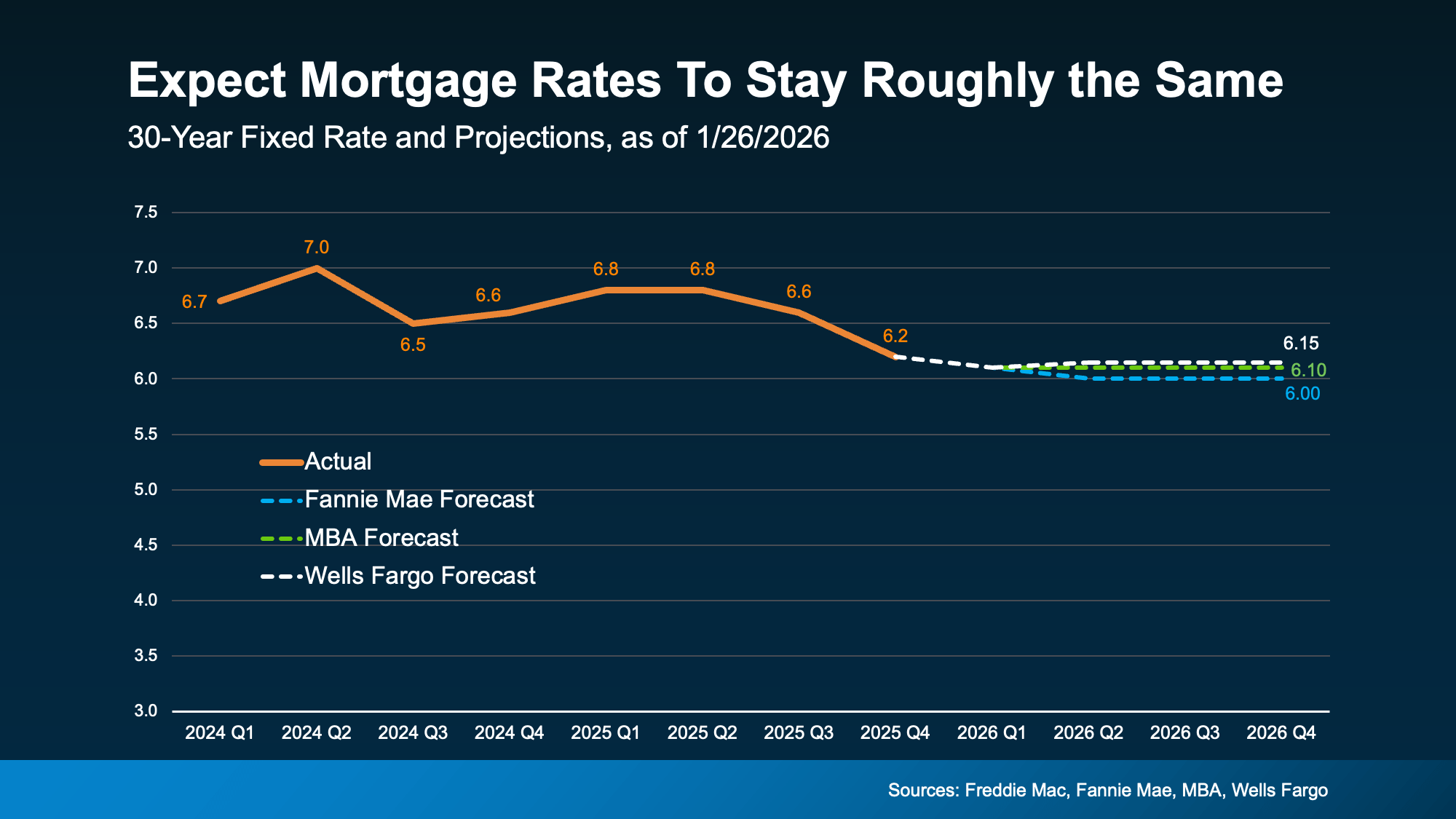

A lot of buyers are hoping mortgage rates will fall even further. But that’s not the best strategy. Here’s why. Experts are pretty aligned on this: rates are expected to stay roughly where they are.

Forecasts throughout the industry all point to the same thing: rates are projected to be in the low-6% range this year (see graph below):

That’s not a bad thing, especially if you consider how much rates have already come down. Over the past 12 months, they’ve dropped roughly a full percentage point. And for many buyers, that means affordability has already improved more than they may realize.

That’s not a bad thing, especially if you consider how much rates have already come down. Over the past 12 months, they’ve dropped roughly a full percentage point. And for many buyers, that means affordability has already improved more than they may realize.

So why wait a few more weeks just for more buyers to jump in and act as your competition? You already have a window right now. As Chen Zhao, Head of Economics Research at Redfin, explains:

“House hunters should know that this may be near the lowest mortgage rates fall for the foreseeable future.”

2. Spring Means More Competition + More Stress

Speaking of competition, the spring market is popular for a reason, but with popularity comes pressure. With more buyers active at that time of year, you’ll have to move faster once you find a home you like. And no one likes feeling rushed.

But buy now and you have more time to browse. Fewer people are looking, so homes sit longer.

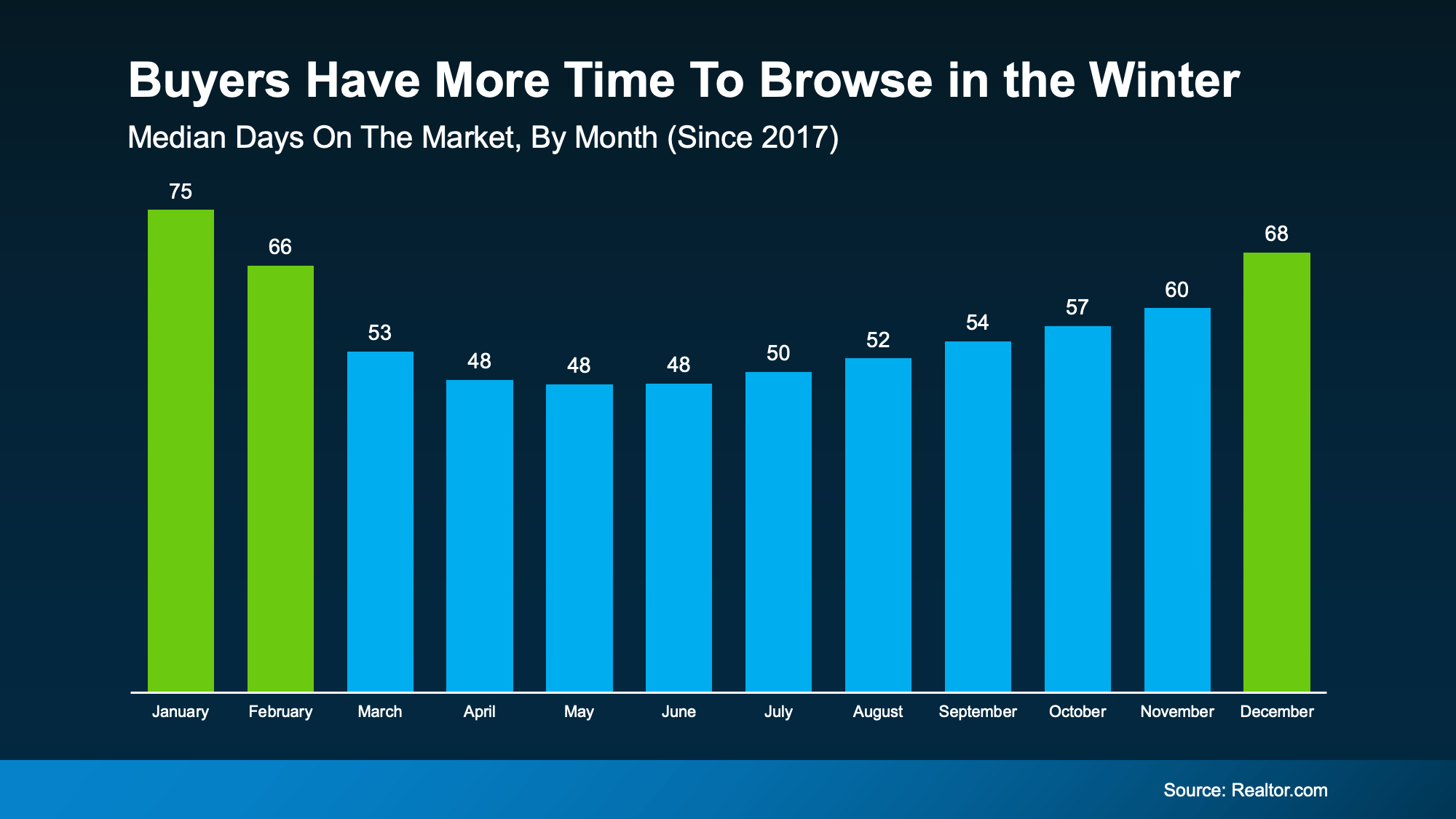

You can see this play out in the data from Realtor.com (see graph below). In winter months, it takes an average of about 70 days for a home to sell. In spring? That drops to about 50 days. That’s a 20-day swing – and that pace is going to be more stressful.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

Homes sell faster in the spring, and slower in the winter. And that can be a worthwhile perk for buyers who want to get ahead before their decisions start to feel rushed.

3. Prices Tend To Rise When Competition Heats Up

And here’s something most buyers forget to factor in. Prices usually respond to demand. So, when demand is higher, prices are too. Bankrate explains:

“Spring and early summer are the busiest and most competitive time of year for the real estate market . . . home prices tend to be steeper to reflect the increased demand.”

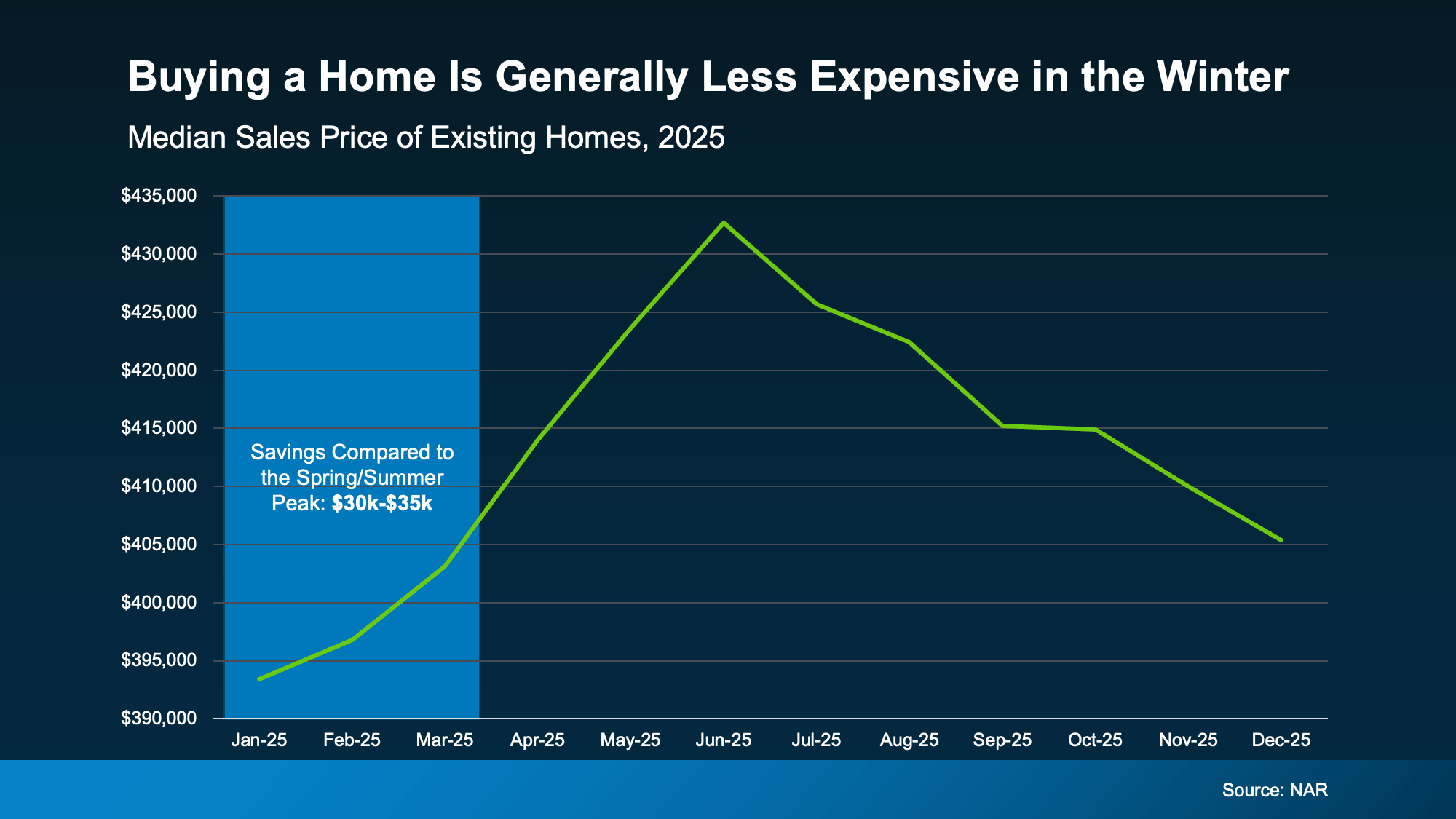

In fact, data from the National Association of Realtors (NAR) shows that in 2025, buyers who purchased in the beginning of the year saved roughly $30,000–$35,000 compared to those who bought when prices peaked in the spring or early summer.

And let’s be honest, for a lot of buyers today, every little bit of savings helps. That’s why buying just a few weeks earlier, before prices ramp up, will be better for you and your wallet.

And let’s be honest, for a lot of buyers today, every little bit of savings helps. That’s why buying just a few weeks earlier, before prices ramp up, will be better for you and your wallet.

Bottom Line

Buying a few weeks before spring isn’t about rushing. It’s about choosing to be ahead of the curve and knowing you want more leverage, less stress, and meaningful savings.

If you’re ready and able to buy now and want to get the ball rolling, let’s connect.

You May Not Want To Skip Over That House That’s Been Sitting on the Market

When you see a house that’s been sitting on the market for a while, the reaction is almost automatic. You start thinking:

What’s wrong with it?

Why hasn’t anyone bought it yet?

Am I missing something?

That mindset made sense a few years ago. But in today’s market, you may actually miss out.

More Time on Market Isn’t Automatically a Concern Anymore

A few years ago, homes sold in just a matter of days. Sometimes, hours. Anything that lingered longer than that raised concerns. But that’s no longer the baseline.

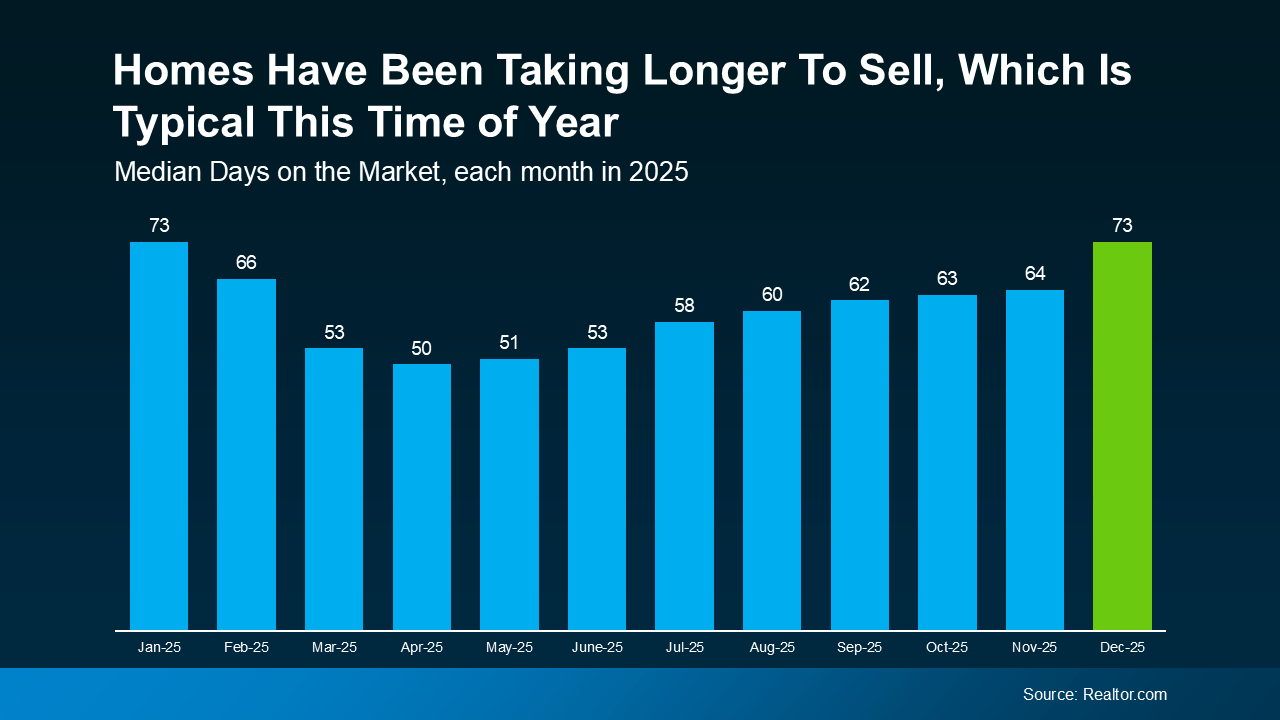

Inventory has grown. Buyers have more choices. And homes are taking longer to sell across the board. Those are some of the reasons why the typical time it takes a home to sell has climbed this year:

a graph of blue barsAnd it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

That shift alone explains a lot of what you’re seeing. It’s not necessarily that there’s anything wrong with the house itself. Although, let’s be honest, sometimes that is the case.

Most of the time today, a house that’s taking longer to sell simply means:

There are a lot of homes for sale in that area

The seller priced a little too high at first

The home didn’t photograph as well online

Buyers passed it over for flashier listings nearby

The timing just wasn’t right when it first hit the market

None of those are necessarily deal-breakers.

What Buyers Often Get Wrong About These Listings

Because even though you may assume a house that hasn’t sold must have hidden issues, the reality is, that’s not always the case. And, if the house does have issues, it’ll show up quickly in your inspection.

That’s information you can use to negotiate. Not a reason to walk away automatically. And in many cases, that’s where buyers find the best deals.

The key is knowing which homes that have been sitting for a while are worth a second look – and which ones aren’t. That’s why working with a local agent makes a real difference. They’ll be able to look at disclosures and more to help you uncover hidden gems other buyers may overlook.

Bottom Line

A home sitting on the market isn’t always a warning sign. Sometimes it’s an overlooked opportunity.

If you want help identifying which homes are worth a second look (and which ones to skip), let’s talk.

Turning a House Into a Home: The Benefits You Can Actually Feel

There’s a lot of conversation about home prices, mortgage rates, and affordability right now – and those things are important. But if you’re thinking about buying a home, it’s worth remembering something the headlines rarely talk about: people don’t buy homes just for financial reasons. They buy them for their lives.

Because while homeownership can absolutely be a smart long-term financial move, it also comes with some emotional benefits spreadsheets just can’t capture. Maybe that’s why a 2025 survey from Fannie Mae notes:

“Consumers were twice as likely to mention lifestyle benefits (67%)—like security, customization, and outdoor space—than financial benefits (34%) when explaining why their homes have become more important in recent years.”

Here are a few reminders of what owning a home gives you that renting never will.

1. A Milestone You Get To Be Proud Of

Buying a home is a big deal. First home, fifth home – it doesn’t matter. It’s a moment you’ll remember. And when you finally get those keys and walk through the door, that feeling of “I did this” hits different. It’s not just a purchase. It’s an accomplishment.

2. A Place That Feels Like Your Reset Button

Life is busy. Having a place that’s truly yours where you can shut the door, take a breath, and settle into your own routine is something renters rarely talk about until they finally experience it. Home becomes the place you go to recharge, not just the place your mail is delivered.

3. Space That Fits the Way You Actually Live

Need a quiet corner for work calls? A backyard big enough for the dog that thinks it’s a person? A shorter drive to see the people who are most important to you? When you own, you get to choose a space that fits your life now and where it’s heading – and it just feels right.

4. Freedom To Make It 100% Yours

Want to paint the kitchen navy? Go for it. Thinking about a wall of floating shelves or a bold wallpaper moment? Do it. Need space for a home gym or a reading nook? Make it happen. Homeownership gives you the freedom to shape your space instead of asking for permission to change it.

Bottom Line

Buying a home isn’t only about dollars and data points – it’s about building a life you love.

So, if you’re thinking about a move in 2026, keep the emotional side in the conversation too. And when you’re ready to explore your options, let’s connect so you have a pro on your side to guide you through the process with clarity and confidence.